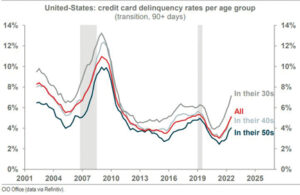

This week’s chart depicts data on U.S. credit card delinquency rates as of June 30th. You will notice a return to pre-pandemic delinquency rates for U.S. consumers overall, however, consumers in their thirties are experiencing the highest delinquency rates since 2011.

Interestingly, this age group also led the trend of higher credit card delinquencies prior to the 2008 Global Financial Crisis. Given we’re currently experiencing the highest interest rates ever for credit cards, we believe delinquencies will continue to increase until interest rates are reduced.

The other consumer-focused interest rates we track, although not at record highs, are at the highest levels in well over a decade – personal loan rates are the highest since Q3 2007, car loan rates are the highest since Q3 2001, and mortgage rates are the highest since Q3 2000.

As discussed in prior articles, monetary policy works with long and variable lags (increasing interest rates eventually slow the economy). Given interest rates are at their most restrictive levels since the 1980s, we continue to see a significant probability of a recession in the U.S.

Canada is already experiencing a technical recession (two consecutive quarters of declining GDP) which could get worse before the Bank of Canada lowers interest rates. After being completely outwitted by inflation in 2021-2022, we expect central banks like the Bank of Canada and the U.S. Federal Reserve to wait until they have overwhelming evidence that inflation has returned to their 2% target prior to cutting interest rates.

This recency bias could lead central banks to leave rates too high for too long to avoid a hard landing for the economy. When we examine the historical length of restrictive interest rate cycles, we see that our current experience isn’t unprecedented.

By our estimates, U.S. rates have now been in restrictive territory for 14 months. Leading into the Global Financial Crisis of 2008, interest rates were restrictive for 25 months and the initial rate cut didn’t occur until 22 months after the Federal Reserve increased rates.

If we use the 2005-2008 experience to attempt to predict the current interest rate cycle in the U.S., we would expect to see interest rates remain restrictive (above 3%) until the fall of 2024 and for the first rate cut to occur next spring.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca