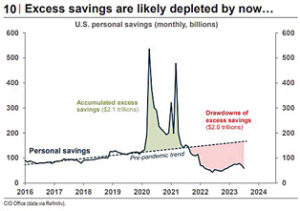

This chart from Refinitiv shows excess savings in the U.S. accumulated during the pandemic.--SUPPLIED IMAGE

Many of the world’s leading economists are scratching their head as to why the North American economy has been as resilient as it has given the largest increase in interest rates since the 1980s.

Economists will highlight the lagged impact of monetary policy – it typically takes 12-18 months for a change in interest rates to be felt by the economy. We’re now at the stage where the impact of significantly higher interest rates should begin to slow the economy. Recall the U.S. Federal Reserve began its current rate hiking cycle in March 2022 (18 months ago). The Bank of Canada started raising rates a few weeks before the Federal Reserve.

As depicted in the supplied chart, a unique feature of the current economic cycle is the impact of excess savings accumulated during the pandemic. In the U.S., a staggering $2.1 trillion in excess savings were accumulated by consumers during the pandemic as they couldn’t spend on dining, travel or entertainment. As you can see from the chart (shown in green), these were additional savings above the long-term savings trend (dotted line).

What I find extremely interesting is the trend which has been in place since restrictions were lifted post COVID (shown in red). As you can see, the massive increase in the savings rate observed during the pandemic completely reversed post pandemic. Furthermore, the $2.1 trillion of excess accumulated savings has been almost fully spent.

Excess savings accumulated during the pandemic created additional spending capacity which helped insulate consumers from inflation. Stated another way, as inflation increased the cost of almost everything, consumers chose to spend savings to maintain their standard of living rather than reduce spending – quite logical behaviour given spending excess savings is less painful than cutting out vacations or eating at restaurants.

The question is what happens to consumer spending now that excess savings have been depleted? Does the substantial increase in mortgage costs, utility costs, food costs, etc. mean the average consumer is running out of money to spend on vacations, restaurants and other discretionary items?

Time will tell, however it seems logical that discretionary spending will be increasingly challenged as consumers have exhausted excess savings and the increase in the basic cost of living consumes a larger percentage of take-home pay. Finally, it’s important to remember the U.S. is a consumer-driven economy, any weakness in consumer spending will quickly be reflected in growth estimates for the largest economy in the world.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca