We receive a lot of questions about Artificial Intelligence focused companies. Specifically, whether the U.S. stock market is in an AI bubble akin to what occurred in the late 1990’s with the dotcom bubble.

Our answer is nuanced as one never knows with 100% certainty if they’re in an investment bubble until after the bubble has burst. There are significant parallels between the current environment for U.S. technology stocks and the last wave of investment in technology associated with the emergence of the internet in the late 1990’s.

Substantial technological breakthroughs such as the internet and AI positively impact the economy by increasing workforce productivity and corporate earnings. If we use the emergence of the internet as our case study, we see it took approximately five years for the impact of increased productivity to be fully realized by the economy.

Annual productivity growth has averaged 1.7% over the past decade in the U.S. If we extrapolate the lag in productivity growth from the internet to the current AI environment, we believe it’s reasonable to foresee U.S. productivity growth above 2.0% for the next decade which positively impacts the economy through lower inflation and higher corporate earnings.

Stock markets are forward-looking, meaning they constantly discount available information and react quickly to changes in earnings and productivity estimates. The current debate as to whether the U.S. stock market is in an AI-driven investment bubble is framed on one side by those who point to relatively high valuation multiples (like we witnessed in the late 1990’s) and those on the other side who highlight the strong and increasing earnings growth of leading AI companies.

There is no debate that the sharp rise in U.S. stock market valuations has been driven by optimism surrounding the impact AI will have on the economy. Ultimately, the winner of this debate will be decided by the impact of AI on earnings growth which won’t be known for some time due to the lagged impact of technological innovation on productivity as described above.

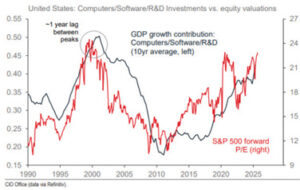

I found this week’s chart interesting because it highlights that U.S. stock valuations (S&P 500 price-to earnings ratios) peaked about a year before spending on IT, software, and R&D peaked during the dotcom bubble. One of my favourite expressions is, ‘history may not repeat, but it often rhymes.’

While parallels between the dotcom bubble and the current environment for U.S. technology stocks exist, there are notable differences. The most significant difference is the strong earnings growth of the largest companies driving AI innovation. Leading AI companies have been able to justify their relatively high valuation multiples by growing earnings at a faster pace than the overall market.

The dotcom bubble burst in the year 2000 when it became evident that most companies with high valuation multiples couldn’t grow their earnings. The chart displays the power of the stock market as a leading indicator as it predicted the peak in technology spending roughly a year before it happened.

Investors reached a point where they were no longer willing to pay high valuation multiples for companies that were expected to grow earnings in the future when it became apparent that earnings growth wasn’t going to occur.

Again, this is where the current market is quite different than the dotcom era as leading AI companies continue to deliver strong earnings growth. The recent messaging from third quarter reporting and guidance is that more investment and AI innovation are expected for 2026 and beyond.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca