Interest rates drive the business cycle and the economy. Lowering interest rates, everything else equal, helps the economy grow by lowering the cost of borrowing, which encourages companies to invest in research, development and hire additional employees.

Lower rates also encourage individuals to borrow money to spend on cars, homes, etc. Increasing interest rates has the opposite effect of slowing the economy. However, central banks like the Bank of Canada and the Federal Reserve in the U.S. aren’t only concerned about economic growth.

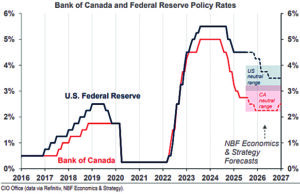

In fact, their primary concern as it pertains to monetary policy is maintaining inflation within a stated range. This week’s chart shows the overnight interest rate controlled by the Federal Reserve in the U.S. in blue and the equivalent overnight rate controlled by the Bank of Canada in red.

Notice the blue and red shaded areas on the righthand side of the chart which represent National Bank Financials’ estimate of the current neutral interest rate range.

A neutral interest rate is theoretical vs. a posted, observable rate and represents the rate which neither encourages nor discourages economic growth. In other words, the neutral rate is an interest rate where the economy is in a steady state of economic growth. If interest rates are lower than neutral, they will cause the economy to expand faster, whereas rates above neutral will cause the economy to slow.

Both the Federal reserve in the U.S. as well as the Bank of Canada reduced interest rates quickly at the start of COVID (2020) as the economy went into recession only to dramatically increase rates as inflation became an issue in 2022. To combat inflation, central banks around the world increased interest rates, which slowed the economy and eventually reduced inflation.

As you can see from the chart, short-term interest rates peaked and began to decline last year in both Canada and the U.S. Notice the current U.S. overnight rate is above our estimate of neutral whereas the current rate in Canada is within our estimate of neutral.

This doesn’t mean interest rates are definitely heading lower in the U.S. or that the Bank of Canada won’t reduce rates further. The actual path of interest rates in both countries will be data dependent.

In other words, both central banks will make their decision based primarily on inflation data. If inflation continues to decline, rates have room to move lower. However, if inflation again becomes a problem for central banks, short-term interest rates may need to be increased.

The dotted blue and red lines on the righthand side of the chart represent our estimate of the near-term path for rates in the U.S. and Canada respectively. Our economics department believes short-term rates will be reduced in both countries with more room to cut rates in the U.S. given their overnight rate remains above our estimate of neutral.

Interestingly, relative interest rate levels are one of the primary factors effecting the value of the Canadian dollar relative to the U.S. dollar.

The current interest rate differential is relatively wide (U.S. rates are substantially higher than Canadian rates) which has contributed to weakness in the Canadian dollar. If the U.S. reduces interest rates closer to prevailing rates in Canada, we may see a corresponding rebound in the value of the Canadian dollar relative to the U.S.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca