When I speak with clients or meet readers of my articles around town, I often receive questions about inflation – what is it and why is it so high? Inflation can be understood through the concept of purchasing power – what you can purchase for $100 at the grocery store today is substantially less than only a few years ago. From an economics standpoint, inflation is neither ‘good’ nor ‘bad’, it is simply a measure of how the prices of a basket of goods and services change over time. Inflation becomes either ‘good’ or ‘bad’ depending on how it impacts the economy and individuals’ lives.

Why do central banks like the Bank of Canada try to maintain inflation near two per cent? Two per cent is somewhat arbitrary; however, the key is economies function best in a goldilocks scenario where inflation is neither too hot nor too cold. Japan represents a recent example of the negative economic impacts of low inflation/deflation. If inflation is too low or negative (deflation), consumers aren’t incentivized to spend money – why would I buy a TV today if I knew it would be cheaper next month? Consumer spending on goods and services represents a significant portion of the economy, thus, low inflation/deflation is negative for economic growth and employment.

At the other end of the spectrum, there are many historic examples of economic disasters created when inflation is too high, post-war Germany, several periods in Argentina, etc. Hyperinflation (very high inflation) is typically caused by large government deficits that encourage the printing of money to repay debt.

However, inflation doesn’t need to reach ‘hyper’ levels to cause damage. Consider the impact inflation has had on the Canadian economy and society since COVID. It’s clear the ‘have nots’ – the poor, the lower-middle class and the youth have been hurt the most by high inflation. The reason is because these groups don’t own enough assets to benefit from inflation.

If you own a house, a cottage, rental property, an investment portfolio, etc., all those assets have increased in value and kept pace with inflation. In many cases, the wealthy and upper-middle class have benefited from higher inflation due to an increase in the value of their assets overwhelming the negative impact of higher goods and services costs.

One of the reasons government deficits contribute to inflation is known as the crowding out effect. If governments run large deficits to pay for expanded government programs like our current federal government, they need to hire additional employees to administer those programs. This creates competition for labour with the private sector which leads to inflation in the labour market.

For example, if an employee is making $60K per year in the private sector and now the government is hiring for a similar role with the added benefits of a pension plan and additional vacation time, how much more does the private sector employer have to pay to keep that employee?

This is one of the great ironies of spending beyond our means – the federal government is hurting the groups it ostensibly wants to assist – the poor, the youth, the ‘have nots’ – by running historically large deficits which are contributing to inflation.

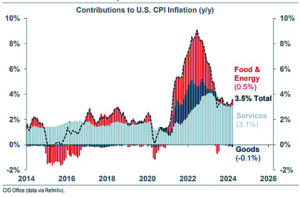

The supplied chart highlights three subsegments of inflation – food & energy (red), services (grey) and goods (dark blue) in the U.S. As is the case in Canada, the U.S. is running massive budget deficits (~6% of GDP). Running this large of a deficit without being in a recession is unprecedented and is contributing to inflation staying above the Federal Reserve’s two per cent target.

As you can see, current inflation is comprised almost entirely by services inflation which is driven by labour costs.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca