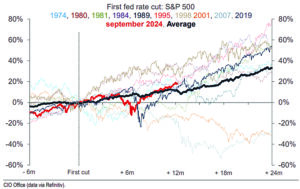

This week’s chart shows the return of the S&P 500 following the U.S. Federal Reserve’s first interest rate cut over ten interest rate cycles since 1974. Notice there are only two observations (2001 & 2007) where the S&P 500 was lower two years after the Federal Reserve’s decision to begin cutting interest rates.

For the other eight observations (1974, 1980, 1981, 1984, 1989, 1995, 1998 & 2019), the S&P 500 was materially higher two years after the first rate cut. In the current cycle (bold red line), we are closely tracking the average of the ten observations (bold black line), approximately one year after the first reduction in interest rates (September 2024).

The average return for the S&P 500 two years following the first interest rate cut by the Federal Reserve is approximately 35% with the highest return approaching 80% (1995 interest rate cutting cycle) and the lowest return of approximately -30% occurring two years after both the 2001 & 2007 interest rate cuts.

The interest rate cutting cycle of 2001 coincided with the bursting of the dotcom bubble. There are significant parallels between the dotcom bubble and the market’s current focus on artificial intelligence. These include the market’s willingness to pay high stock valuation multiples on the expectation of future earnings growth and the high concentration of the value of the S&P 500 being attributed to a handful of companies (Magnificent 7 in the case of artificial intelligence).

However, there are very important differences between the dotcom bubble and the current artificial intelligence driven market; primarily, the ability of the Magnificent 7 group of companies to grow into their earnings multiple.

In other words, the large U.S. technology companies which currently represent a substantial share of the S&P 500 have been able to grow their earnings at rates which have, thus far, met or exceeded market expectations. This was not the case in the dotcom bubble when many of the largest dotcom companies were never able to generate positive earnings.

2007 is the other observation with a negative return two years after the first rate cut, however, that cut immediately preceded the Global Financial Crisis of 2008 which became the worst recession experienced since the 1930’s.

The Global Financial Crisis of 2008 was primarily caused by mortgage fraud and excessive leverage associated with mortgage-backed securities which ultimately created a liquidity crisis in the U.S. banking system.

A well-known market saying is, “the trend is your friend” which simply means investors should continue to follow trends until those trends have been broken. This is also known as momentum investing, which isn’t a method of investing that I subscribe to, but many successful investors do.

Another well-known saying among capital market participants is, “don’t fight the Fed” which means the market will most often do what the U.S. Federal Reserve wants it to do.

If the U.S. Federal Reserve is cutting interest rates and / or providing the market with stimulus, the stock market typically responds favorably. Currently, the Federal Reserve is in an interest rate cutting cycle and the trend of the S&P 500 is higher.

Eric Van Enk is a wealth adviser & associate portfolio manager with National Bank Financial in Medicine Hat. He is a graduate of the University of Calgary, as well as a CFA charter holder with 20 years of financial markets experience in New York, Toronto and Calgary. He can be reached at eric.vanenk@nbc.ca